Research: Karen Chapple and Byeonghwa Jeong

Graphics: Scott McCallum, Byeonghwa Jeong, Jeff Allen

As the COVID-19 pandemic waned, economists began writing about a “flight to quality,” the phenomenon whereby new commercial office buildings with more amenities are able to maintain net effective rents even as rents decline on new leases in older buildings. These green, energy-efficient buildings typically include not only top-notch facilities such as high-tech elevators, 24/7 security, high ceilings, and concierge-level services, but also outdoor terraces, cafes, and leisure facilities. In some cities, so-called “A+” buildings are seen as the only real hope for the office construction sector.

As part of our Downtown Recovery Project, we began wondering whether we could corroborate this flight to quality using footfall data. If this “flight” is indeed occurring, we should see consistently more activity (as measured by cell phone data) at these A+ buildings than in the rest of the commercial office market.

So we took a deep dive into activity patterns at the 249 highest quality office buildings across the U.S. and Canada in a new paper. We identified A+ buildings using CoStar data, selecting those with star ratings of 5. We then compared their activity levels in March-June 2023 to the pre-pandemic period, March-June 2019 (i.e., the recovery rate used in our rankings).

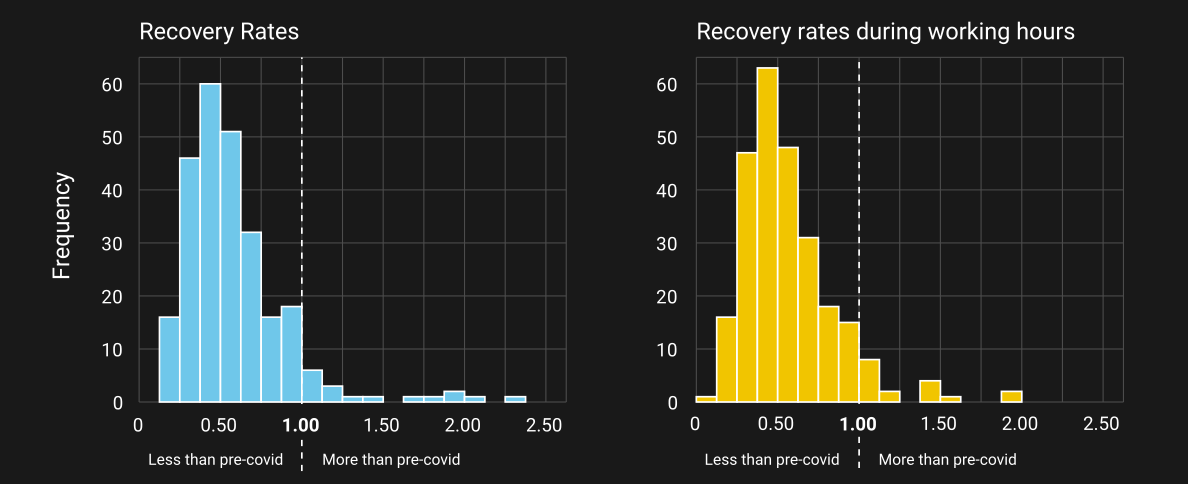

What we found surprised us. Even among the highest quality buildings in U.S. and Canada, recovery is lagging, and there is great diversity in activity levels. Figure 1 shows recovery rates throughout the week (left panel) and during working hours only (Monday-Friday, 8 AM – 6 PM) (right panel). The mean recovery rate among these buildings is 56% overall and 55% during working hours, compared to 77% and 78% for all buildings. Recovery rates for individual buildings range from 15% to over 200%.

What accounts for the poor performance of these buildings? Well, even if rents are high, some are experiencing high vacancy rates; though the mean vacancy rate is just 12%, it ranges up to 68%, suggesting that some buildings are emptying out.

But might the incidence of work-from-home be impacting performance as well? In our research, we find that overconcentration in specific economic sectors (primarily professional services and information technology) is driving low footfall in downtowns. So for this study we next analyzed the type of tenants occupying A+ buildings. We classified industries based on their potential for remote work and identified the occupied square feet by each category. For example, we classified professional, scientific, technical services, and information technology as remote work; educational services, health care, and social assistance as hybrid work; and construction and transportation as traditional, in-person work.

Indeed, we found that the highest quality office buildings tend to have a very high concentration of space housing remote work sectors – a mean of 70%. Hybrid and traditional work sectors are under-represented in these buildings. This means that most workers in those buildings tend to work remotely, which is likely to decrease the demand for office space.

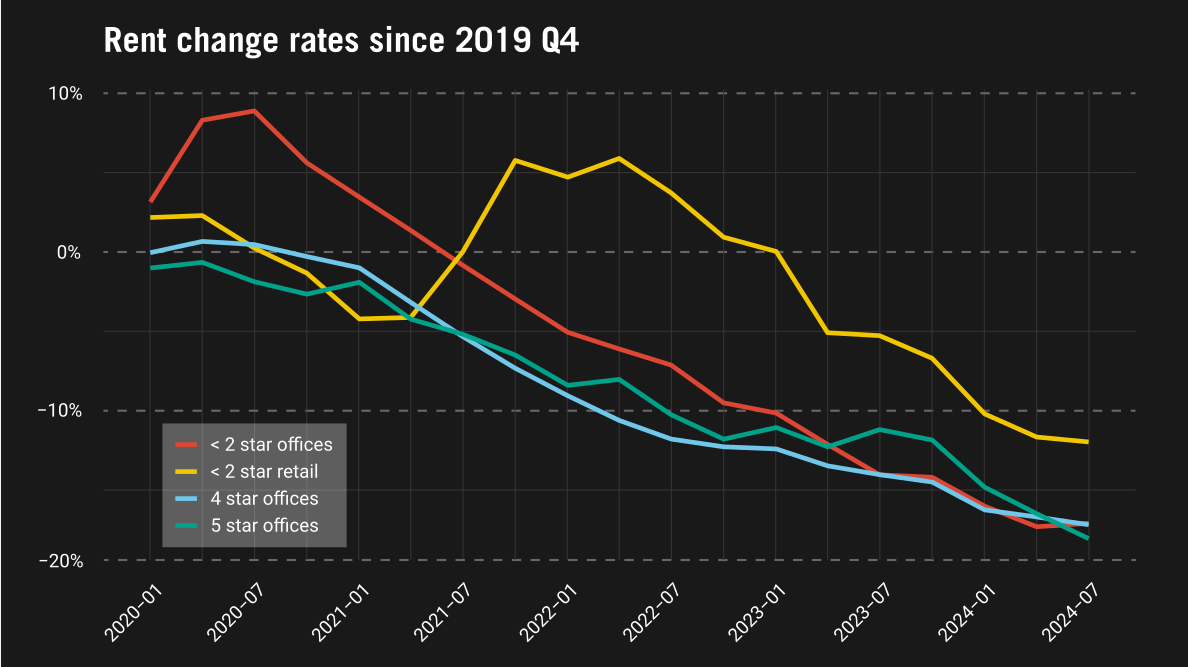

These findings led us to investigate further the rent dynamics in downtown office buildings. Looking at the change in rent per square foot (inflation-adjusted) relative to the pre-pandemic period, we see declines across the office building sector (Figure 2). Five-star buildings have indeed seen occasional upticks, but in general, the trajectory is negative. In fact, rents for 5-star offices have declined 19% since before the pandemic – more than 4-star or 2-star office buildings, or even 2-star retail facilities. These rent declines corroborate our findings of poor recovery rates, and undermine the concept of a flight to quality.

Thus even if high rent levels in new leases suggest a flight to quality, it seems probable that buildings with an overconcentration of tenants relying on remote work are not fully utilizing their space. With large numbers of employees coming to work only a few days a week, and specialization in sectors relying on remote work not likely to change, even the highest quality buildings are struggling. Many commercial leases will be renegotiated or terminated over the next five years – but with inconsistent activity levels as described here, even the future of A+ buildings remains uncertain.